How to Calculate a Capital Gain or Loss

TurboTax Canada

February 6, 2025 | 1 Min Read

Updated for tax year 2025

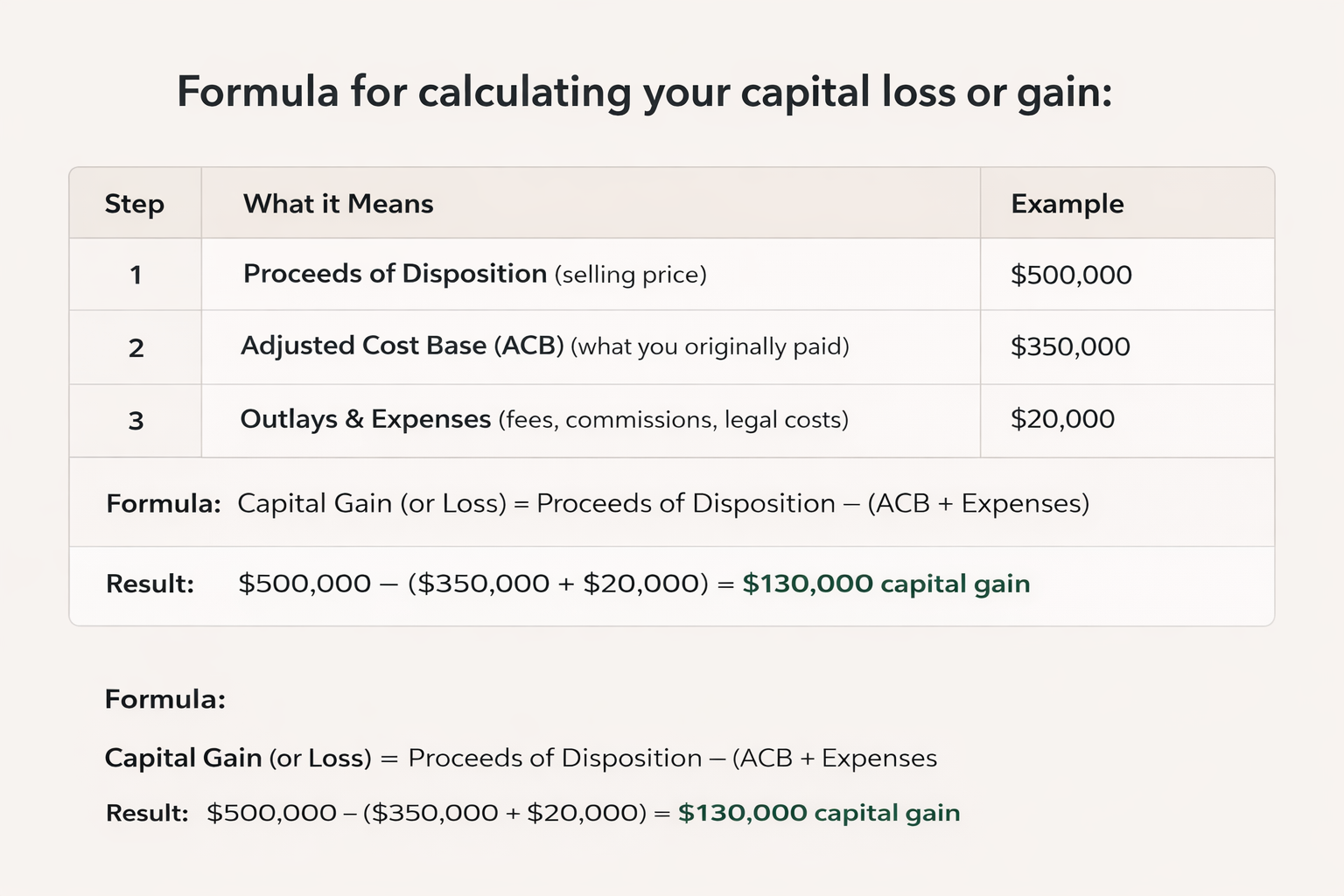

When you have a capital gain or loss, you figure out how much of a gain or loss you have by subtracting your buying price from your selling price. Or, expressed in tax terminology, you subtract the total of the property’s adjusted cost base and any outlays and expenses incurred to sell your property from the proceeds of disposition.

Let’s look at some definitions

- First, the proceeds of disposition are the amount of money you received for your property (the selling price).

- The outlays and expenses are basically your costs for selling the property. For instance, you may have had to repair some things on the property before you could sell it, or pay brokers’ or surveyors’ fees. Legal fees and the cost of advertising your property in order to sell it are included in this category.

- The adjusted cost base (also known as ACB) of your property is generally what it cost you to buy the property (the cost of the property plus any expenses to acquire it, such as legal fees).

Capital Gain vs. Capital Loss

- If you sell capital property for more than you paid for it, the resulting portion added to your net income is a capital gain.

- Conversely, if you sell capital property for less than you originally paid for it, you may have a capital loss.

Note that the actual or deemed cost of a capital property depends on the type of property and how you acquired it, and includes capital expenditures, such as the cost of additions and improvements to the property, but not current expenses.

Here’s an example calculation resulting in a capital gain:

Suppose you had a rental property that you received $380,000 for when you sold it and had originally purchased for $320,000. When you bought the property, you paid legal fees of $2,600. Before you sold it, you had to have the back deck of the house replaced which cost you $4,000 and the sale of the property cost you $1,500 in legal fees.

Your calculation of capital gain or loss would then be:

Proceeds of disposition $380,000

Adjusted cost base $322,600

+

Outlays and expenses $5,500

________________________

$328,100

$380,000 – $328,100 = $51,900 = a capital gain

If You Have a Capital Loss Rather Than a Capital Gain

- If applying the formula for calculating a capital gain or loss results in a loss rather than a gain, you can use your capital loss to reduce any capital gains you had in the year, all the way down to zero if you have enough of them.

- If you have even more than that, you’ll be happy to know that a net capital loss can be applied to any taxable capital gains you’ve had in the three preceding years and to taxable capital gains of any future years.

Income tax form-wise, all of your capital gains and/or losses are calculated and reported on Schedule 3, Capital Gains (or Losses), even if your capital gains or losses are related to using a property for business purposes.

TurboTax has helped millions of Canadians file for Free! Try TurboTax Free with no income limits. For more info on TurboTax Free, click here.

Related articles

© 1997-2024 Intuit, Inc. All rights reserved. Intuit, QuickBooks, QB, TurboTax, Profile, and Mint are registered trademarks of Intuit Inc. Terms and conditions, features, support, pricing, and service options subject to change without notice.

Copyright © Intuit Canada ULC, 2024. All rights reserved.

The views expressed on this site are intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.