With Expert 365, get expert help cleaning up your books for tax time, plus support on sales tax and payroll reporting year-round.

T2 Corporation Income Tax Return

TurboTax Canada

February 28, 2020 | 3 Min Read

Updated for tax year 2025

A new way to file your business taxes is here!

Filing a T2 Corporation Income Tax Return can be easy—with the right guidance. Whether you're a seasoned business owner or new to corporate taxes, understanding the process is crucial.

In this guide, we'll walk you through who needs to file, the types of T2 tax returns available, key deadlines, and how to file efficiently.

Key Takeaways

- All Canadian corporations must file a T2 tax return within 6 months after their fiscal year-end—even if no taxes are due.

- The T2 Short Return is a simplified filing option for eligible corporations, including certain Canadian-controlled private corporations (CCPCs) and tax-exempt organizations.

- Using CRA-certified software like TurboTax Business can simplify filing, ensure accuracy, and help you stay compliant with CRA requirements.

What is a T2 Corporation Income Tax Return?

The T2 Corporation Income Tax Return, also referred to as a "declaration of corporate income," is a form that must be filed by all Canadian resident corporations to report their income and file taxes.

Corporations in Canada must file a T2 tax return each year, just like individuals must file personal returns. The Canada Revenue Agency (CRA) provides the T2 tax return specifically for corporations to ensure compliance and accurate corporate tax filing. (If your corporation is in Alberta or Quebec, you will also have to file a provincial form in addition to the federal form.)

How do you get a T2 online?

One way to obtain a T2 tax return online is by downloading it from the CRA's official website. The CRA offers fillable PDF versions.

But TurboTax offers a streamlined way to prepare and submit your T2 online. Designed specifically for Canadian corporations, TurboTax Business Assisted can file your T2 tax return with efficiency and ease.

While electronic filing is mandatory for most businesses, certain corporations may still access the T2 form through other means if necessary. These include:

- Order by telephone. Call the CRA at 1-800-959-5525 (Canada and U.S.) between 9 a.m. and 5 p.m. local time, Monday to Friday. For international calls, dial 613-940-8497; collect calls are accepted through a telephone operator.

- Alternate access. For individuals with visual impairments, the T2 form is also available in different formats, such as MP3, braille, large print, and electronic text.

Who needs to file a T2 Corporation Income Tax Return?

Most corporations in Canada are required to file a T2 tax return annually, even if no tax is payable. This includes resident corporations, such as Canadian-controlled private corporations (CCPCs), non-profit organizations, tax-exempt corporations, and inactive corporations. The only exceptions are tax-exempt Crown corporations, Hutterite colonies, and registered charities.

Non-resident corporations must file a T2 return if they carried out business in Canada, had a taxable capital gain, or disposed of taxable Canadian property during the year.

When can the T2 Short Return be used?

The T2 Short Return is a simplified version of the standard T2 Corporation Income Tax Return, designed for corporations that meet certain criteria. Eligible corporations include:

- CCPCs with nil net income or a loss throughout the tax year

- Non-profit organizations or corporations exempt from tax under Section 149 of the Income Tax Act

To qualify, the corporation must also:

- Have a permanent establishment in only one province or territory.

- Not claim any refundable tax credits.

- Not pay or receive taxable dividends.

- Report exclusively in Canadian currency.

- Not have an Ontario transitional tax debit. This refers to tax adjustments related to the transition from Ontario's previous corporate tax system to the federal system. Corporations with such debits are required to file additional schedules and are not eligible for the T2 Short Return.

- Not report a Section 34.2 amount, which applies to corporations involved in partnerships whose business year doesn't match the corporation's own tax year. Tax declarations for these corporations require extra steps, which makes them ineligible for the T2 Short Return.

When is the corporate tax filing deadline?

Filing the T2 tax return on time is essential to avoid penalties and interest charges. Corporations must file their T2 return within 6 months after the end of their fiscal year. For example, if the fiscal year ends on December 31, the filing deadline is June 30 of the following year. If the fiscal year ends on a day other than the last day of the month, the return is due on that day 6 months later.

Any corporate taxes owed are generally due within 2 months after the fiscal year-end. However, certain CCPCs may have up to 3 months to pay, depending on specific conditions. If you pay your corporate taxes in installments, you may not have to worry about paying a lump sum at the end of the year.

If a filing or payment deadline falls on a weekend or statutory holiday recognized by the CRA, the return or payment is considered on time if received or postmarked on or before the next business day.

Failing to file the T2 return by the due date can result in a penalty of 5% of the unpaid tax, plus 1% for each full month the return is late—up to a maximum of 12 months.

How do you file a T2 return electronically?

Electronic filing is mandatory for most corporations for all tax years starting after 2023. This steps below outline the process for ensuring accurate corporate tax filing and compliance with CRA regulations:

Stefanie Ricchio

CPA and TurboTax tax expert

1. Gather necessary information

- Financial statements. Prepare the income statement, balance sheet, and cash flow statement. Accurate bookkeeping is essential, as these documents correspond to specific schedules within the T2 tax return, including Schedule 100 (Balance Sheet) and Schedule 125 (Income Statement).

- Business number. Ensure the corporation's unique business number assigned by the CRA is available.

- GIFI codes. Utilize the General Index of Financial Information (GIFI) codes when preparing financial statements. Each item corresponds to a specific GIFI code.

2. Complete the T2 return

- Identification. Provide your corporation's name, business number, and fiscal period.

- Income and deductions. Report all income sources and claim any applicable deductions or credits. Our small business tax experts will help you uncover each deduction or credit your business is eligible for.

- Tax calculation. Calculate the net tax payable or refund due.

3. Review and submit

- Accuracy check. Before submitting your T2 return, it's essential to ensure all information and balances submitted are accurate to avoid delays or penalties. A TurboTax business tax expert can perform a thorough review of all returns submitted to ensure complete compliance with CRA requirements.

4. Payment of taxes owed

- Due date. Any balance owing is typically due within 2 or 3 months after your fiscal year-end, depending on your corporation's specifics.

- Payment methods. Payments can be made online, at your financial institution, or by mail.

5. Maintain records

- Retention period. Keep all tax records and supporting documents for at least 6 years in case of a CRA review or audit.

For filing support, TurboTax Business can provide guidance, built-in checks to highlight missing information and inconsistencies, and immediate confirmation upon submission.

How to simplify your corporate tax filing

TurboTax Business is an easy way to submit a T2 tax return for both experienced business owners or new entrepreneurs. It offers:

- User-friendly interface. Step-by-step guidance simplifies the T2 filing process.

- Compliance. Built-in checks to minimize mistakes, ensure compliance, and avoid penalties.

- Maximize your deductions. Be tax efficient, so you keep more money in your company.

- Experts on hand. TurboTax's team of business Canadian tax professionals are available to help you with any questions related to the T2 tax return as you prepare it.

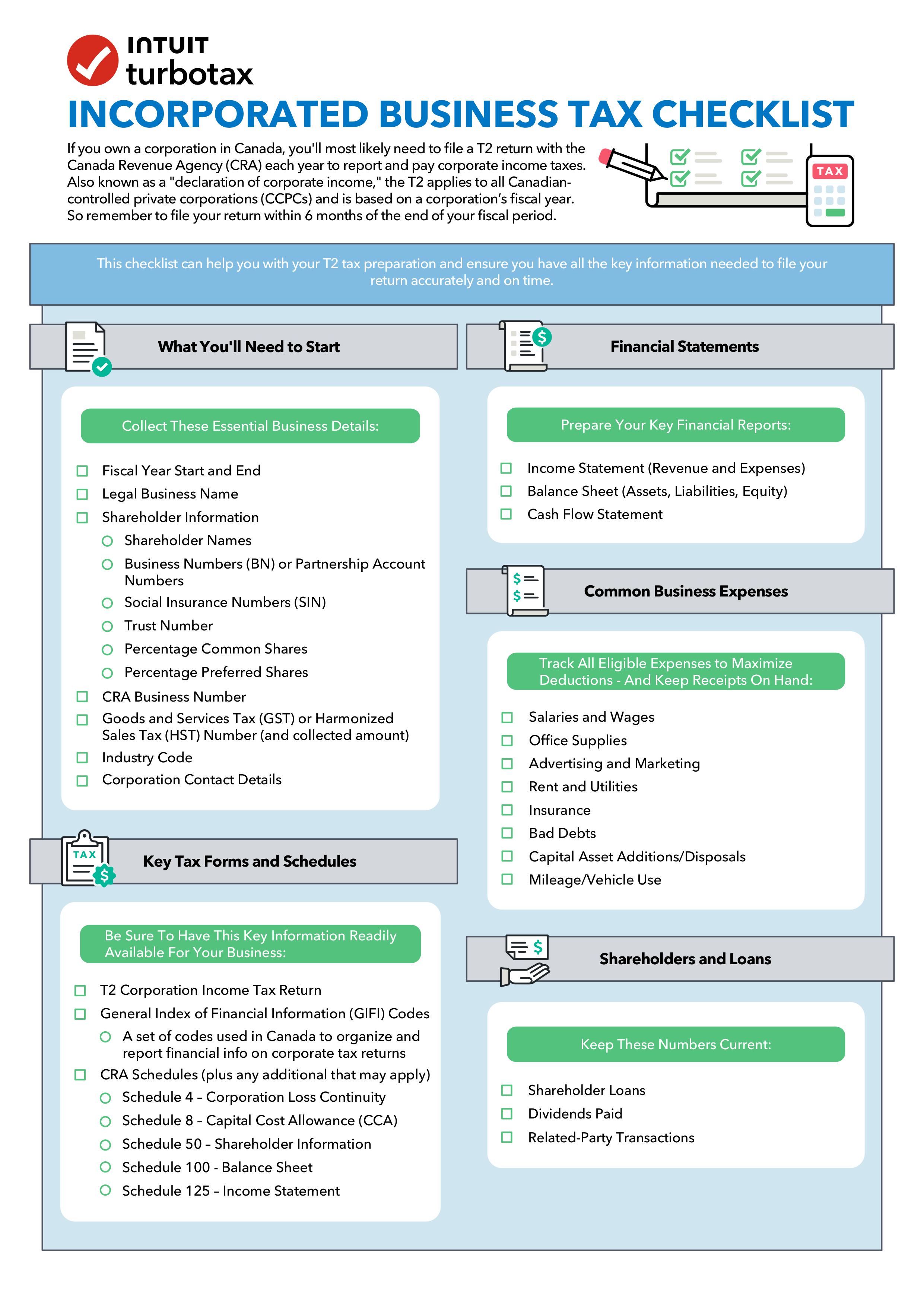

What documents do I need to file my corporate taxes?

When you file your taxes online you will need certain forms and supporting documents to complete your return.

The ultimate checklist to file your corporate taxes

Get organized to confidently tackle your taxes. This tax checklist tells you everything you need to file your corporate return on time and accurately.

Download Checklist

Filing your taxes in Canada can be straightforward—even with corporate T2 returns.

Use TurboTax Business, a CRA-certified tax software, to file your T2 returns with ease. You’ll get help and guidance while you prepare your return, plus a final review before you file—so you’re never on your own. TurboTax also can offer expert year-round help with your corporate GST/HST questions and returns, as well as other bookkeeping help and payroll questions.

What is a T2 Corporation Income Tax Return?

Who needs to file a T2 Corporation Income Tax Return?

When can the T2 Short Return be used?

When is the corporate tax filing deadline?

How do you file a T2 return electronically?

How to simplify your corporate tax filing

What documents do I need to file my corporate taxes?

Filing your taxes in Canada can be straightforward—even with corporate T2 returns.

© 1997-2024 Intuit, Inc. All rights reserved. Intuit, QuickBooks, QB, TurboTax, Profile, and Mint are registered trademarks of Intuit Inc. Terms and conditions, features, support, pricing, and service options subject to change without notice.

Copyright © Intuit Canada ULC, 2024. All rights reserved.

The views expressed on this site are intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.