Canadian Income Tax Rates Are the Same for Sole Proprietors and Employed Individuals.

When you are self-employed as a “sole-proprietorship” there is actually no difference between you and your business as far as the Canada Revenue Agency (CRA) is concerned. All money you earn in the business goes towards your total income earned on line 15000. What this means is that the income tax rates for sole-proprietors are the same as for individuals.

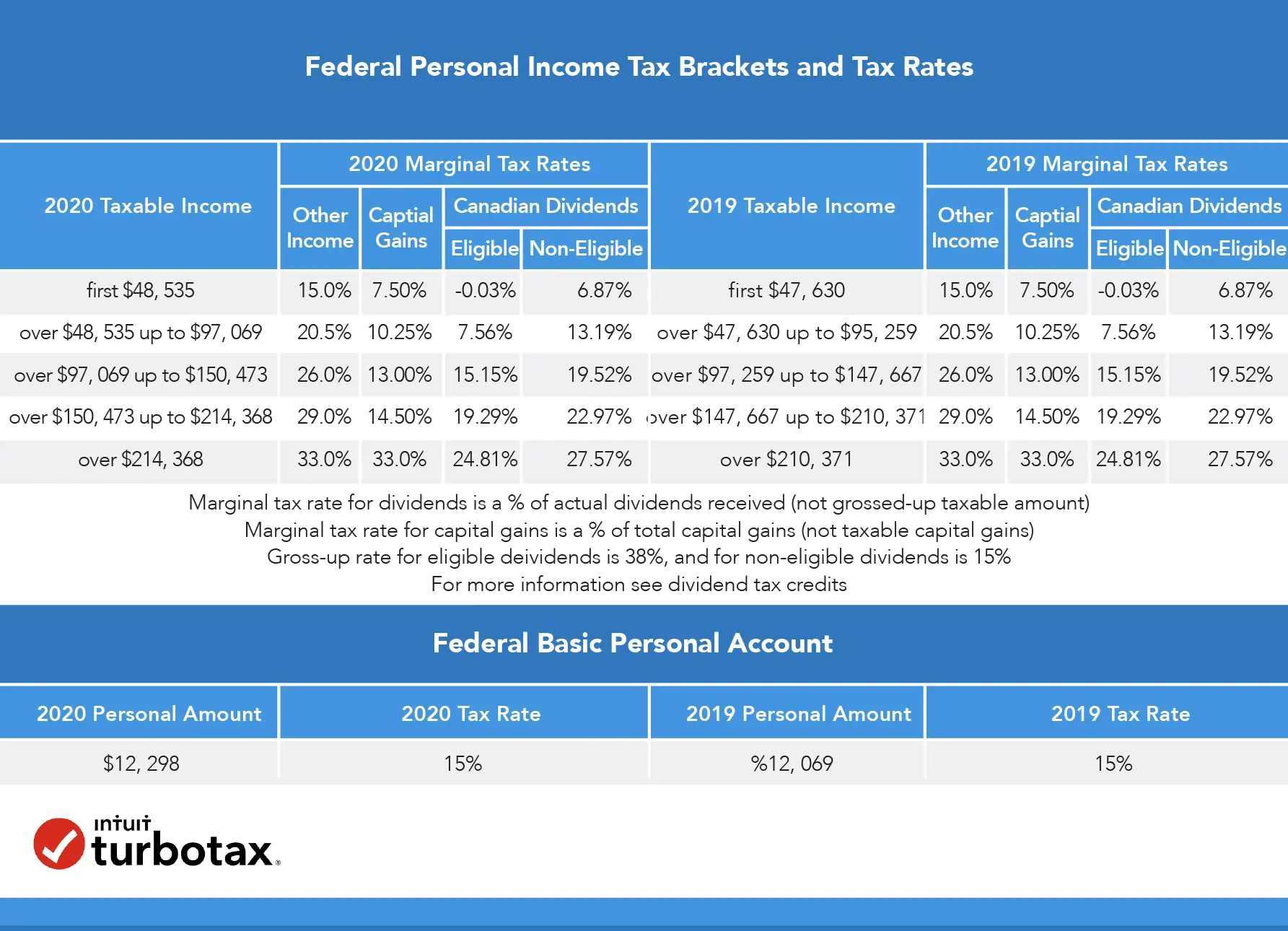

Tax rates for self-employed Canadians

Self-Employed Canadians Can Claim Business Expenses

“The CRA allows self-employed individuals to claim a host of expenses provided they are used to generate income and are reasonable,” explains Ronald Watson, chartered accountant in Fort Erie, Ontario. “Income tax rates for the self-employed individual are the same as personal tax rates for employed workers. With a small difference,” Watson adds. “Someone who owns their own business has deductions that are more than the average wage earner.”

- The income earned from self-employment can be from a sole proprietorship or a partnership.

- However, if your business is incorporated, it is not considered a self-employment situation.

2020 Federal Income Tax Rates for Self-Employed Canadians

If you’re self employed as a sole-proprietorship or partnership, you must file your personal income tax return and pay the same amount of tax as any employed wage earner. Your business income, after deductions, is considered your annual wage, you report it as professional or business income on a T2125 form.

- 15% on the first $48,535 of taxable income, plus

- 20.5% on the next $48,534 of taxable income (on the portion of taxable income over $48,535 up to $97,069), plus

- 26% on the next $53,404 of taxable income (on the portion of taxable income over $97,069 up to $150,473), plus

- 29% on the next $63,895 of taxable income (on the portion of taxable income over $150,473 up to $214,368), plus

- 33% of taxable income over $214,368

Don’t forget to consider the Provincial Tax Rates

Each province and territory in Canada (other than Quebec), have provincial/territorial tax that is levied (collected) by the CRA.

If you’re curious about your province, go to the Provincial and territorial tax rates section.

Definition of a Business For Income Tax Purposes

The definition of a business under Canadian tax law is “a profession, calling, trade, manufacture, undertaking of any kind whatever or an adventure or concern in the nature of trade.” It must be entered into with a reasonable expectation of turning a profit, and there must be evidence to that extent. The profit you generate from any activity is considered business income and must be declared. A business must also have a definite start date. You can deduct expenses against the profit as of this date. CRA reviews each business on its own merits when defining the business’s start date.

Claiming Business Expenses

“When it comes to claiming expenses against your business income,” Watson notes, “There’s a very broad brush stroke that can be used. Anything that I use to make a profit is potentially deductible.” The CRA allows a multitude of business expenses to be deducted from salaries and benefits, traveling expenses, goods for retail sale, attorney and accounting fees, rent, leases, bank charges and maintenance. If your business is located in your home, you can deduct portions of your mortgage payments, rent, utilities, repairs, upgrades and property tax. The percentage deducted depends on the amount of space you use to carry on your venture. Car expenses may be deductible if you use your car to do business, including lease payments, maintenance, parking and depreciation of the vehicle. All of these deductions help reduce your taxable income and thereby your taxable rate.

You can check the TurboTax link on Business Deductions for more information.

Filing as A Partnership

A partnership does not file income tax on its earnings and is not required to pay tax. The income earned from a partnership is divided between the partners, and each respective partner files her own return. The income, deductions and any other credits or losses are divided according to the partnership agreement in place. Each share of income must be reported whether it was received in cash or as a credit. Special rules apply to a partnership concerning capital gains and losses and recapturing cost allowance. If a partnership is dissolved or an interest is sold or disposed, CRA has special guidelines in place.

COVID Impact on Self-Employment

Many businesses have been impacted by the COVID pandemic. Self-employed taxpayers are facing challenges with financing, managing from distance, leasing, paying employees, etc. CRA offers COVID incentives to support your business during this difficult time whether through CERB, CEWS, or CEBA.

If your earned income in the 12 months prior to applying for Canada Emergency Response Benefit (CERB) was at least $5,000, you will be receiving a taxable benefit of $2,000 every 4 weeks as long as your income within the 4 weeks is less than $1,000. If you need further help to apply for an interest-free business loan, you should consider the Canada Emergency Business Account option (CEBA).

CRA provides another benefit called the Canada Emergency Wage Subsidy (CEWS) to cover a portion of your employees’ wages to avoid layoffs.

If you are renting a space for your small business, you might want to discuss deferring rent payments with your landlord. The government had panned eviction during the pandemic to support renters in most provinces. CRA also provides help through Canada Emergency Commercial Rent Assistance (CECRA) to cover a portion of the rent for small business owners.

For more information about other Emergency Responses from CRA, please visit their link.

Turbo Tax Self-Employed helps you easily manage your sole-proprietorship business earnings and expenses. However, if you feel a bit overwhelmed, consider TurboTax Live Assist & Review, Self-Employed, and get unlimited help and advice as you do your taxes, plus a final review before you file. Or choose TurboTax Live Full Service for Self-Employed and have one of our tax experts do you return from start to finish.

References & Resources

- Canada Revenue Agency: Employee or Self-Employed?

- Ronald Watson; Chartered Accountant; Fort Erie; Ontario

- Canada Revenue Agency: Sole Proprietorships and Partnerships

- Canada Revenue Agency: Canadian Income Tax Rates for Individuals – Current and Previous Years

- Canada Revenue Agency: What is a Business?

- Canada Revenue Agency: Reporting Partnership Income

- Canada Revenue Agency: T5013 Partnership Information Return Filing Requirements