With Expert 365, get expert help cleaning up your books for tax time, plus support on sales tax and payroll reporting year-round.

5 Tips for Being a Business Bookkeeping Pro

TurboTax Canada

May 22, 2025 | 5 Min Read

Updated for tax year 2025

A new way to file your business taxes is here!

Running a business, as those that do know, can be sweaty. There are so many factors that are at play to not only keep the doors open but to get to the level of success you’re looking for. Many that run businesses look at their accounting records as something that needs to happen just for tax time, however, compliance is only one part of why you need to manage the bookkeeping for your business year-round.

What is “compliance”? Compliance is what we must do in order to satisfy certain rules or laws regarding business ownership, such as adhering to tax legislation.

Consider things like:

- Collecting and remitting sales taxes (GST/HST/PST or QST)

- Filing business tax returns, whether a sole proprietor, a partnership or a corporation (and paying any income taxes that come along with that).

- If you have employees, compliance responsibilities includes:

- Withhold CPP, EI and income taxes from their pay cheques

- Send them to the CRA monthly

- Create those very important T4 slips each February.

The other main reason for managing your business finances is so that you can understand how the business is performing. Simply put, if you don’t track the money, how do you know you’re making any?

If we’re not looking at our business accounting records so we can pay taxes or file an HST return, what are we looking at and why does it matter?

Here are 5 important things your accounting records are going to tell you about your business’ performance.

Key Takeaways

- Bookkeeping compliance responsibilities includes withholding CPP, EI and income taxes from their pay cheques and sending them to the CRA monthly, and creating T4 slips every February.

- Understand how your business is performing by keeping track of invoices and expenses, reviewing financial reports, and organizing your receipts.

- Using tools like QuickBooks and reviewing financial reports makes it easier to stay organized and prepare for tax time.

1. Know how much money you are making

When you invoice a client for your services or product, you are actually doing your bookkeeping, especially if you’re using software like QuickBooks Online to help you. Tracking your income will show you what you’ve billed your customers over a period on specific items or groups of items called “revenue streams”.

Why is this important to know? As you track your income, you will easily see what items or services you are selling the most of; for those where you are not selling enough, you can use this information to help you determine if you keep this product/service, advertise it more, or perhaps reconsider its selling price.

2. Understand what are your costs are

For many businesses there is a direct cost to making a sale; these are also known as cost of goods sold or variable costs. That means that to sell your product for $50, for example, it might have required you to buy $10 in materials and spend $20 in labour. Without spending that $30 you never wouldn’t have had a product to sell. The resulting gross profit in this example is $20.

Why is this important to know? Tracking costs against revenue will allow you to calculate your Gross Profit; what is it costing you to make/sell your product?

Gross profit = Total Revenue – Total Direct Costs

By knowing your gross profit, you can determine if you need to reduce your costs. The gross profit is what is left for you to pay for everything else in your business, that is not related to your output, which are your fixed costs.

3. Define your operating expenses

All businesses have operating costs that they must pay for regardless of whether they are selling any goods or services. Fixed expenses are costs that remain constant regardless of how much you sell. Here are some common of fixed expenses that businesses typically incur:

- Advertising

- Office expenses

- Rent

- Insurance

- Salaries

- Utilities

- Depreciation

- Property taxes

These expenses have no direct tie to your business’ income (yes, even though advertising may help you make sales). Even if you make no money, you still have these costs to bear.

Why is this important to know? As mentioned in the last section, the amount of money you have for these fixed expenses is your gross profit amount. What happens if there isn’t enough of a gross profit to afford these costs? Knowing what you need to spend money on to operate your business, along with your direct costs, will assist you in determining how to price your products and how much you need to sell to earn what you need to stay afloat.

4. Know your bottom line

After all of the above numbers are calculated, this is your bottom line. Are you earning money each period or are you losing money?

Why is this important to know? The purpose of running a business is to earn a profit – that is actually the definition as per the CRA. Some businesses will see a loss in the first couple of years of operation as there are often costs that need to be outlayed before any income can be generated. However, if over time, the business is not earning the profit you want it to be, then there is a reason and you will need to look at all the numbers above, and why they’re important, to help you resolve it. Part of any business’ success is the viability of that business; is this a business that can survive, cover its own costs and turn a profit?

Those are just some of the details you can get out of your business’ financial records and how they can help you. If you are currently not tracking your finances and often just drop off all your receipts at the accountant’s office at tax time you should consider the benefit of knowing this information throughout the year. No one wants to know what they should have been doing all year when you can’t change it; by managing your finances throughout the year you can address issues head on.

5. Be the master of your books

There are lots of ways to track your finances, but one of the easiest ways is to have an online system in place to track everything from your income to your expenses and even your sales taxes. Software like QuickBooks Online make it easy to invoice your clients and deal with all of your expenses as they happen.

Here are some best practices to help you you stay organized year-round:

- Review financial reports on a regular basis. By tracking your income and expenses you will be able to create financial reports, such as your Profit and Loss statement, that shows you the performance of your business during a period.

- Have a plan to deal with your receipts frequently. Set up an administrative time for you each week for example, and focus on inputting everything into your accounting system. Make it a habit so that if you need the information on short notice, you will be able to quickly retrieve it.

- Organize your income and expenses. Using an online bookkeeping system can help automate much of what you need for business and sales tax returns. And having everything organized and ready to go may enable you to do your own business taxes, saving money and time in the process. Tax time will become much easier.

- Have questions? TurboTax can help with your return as well as offer expert year-round help with your corporate GST/HST questions and returns, and other bookkeeping and payroll help.

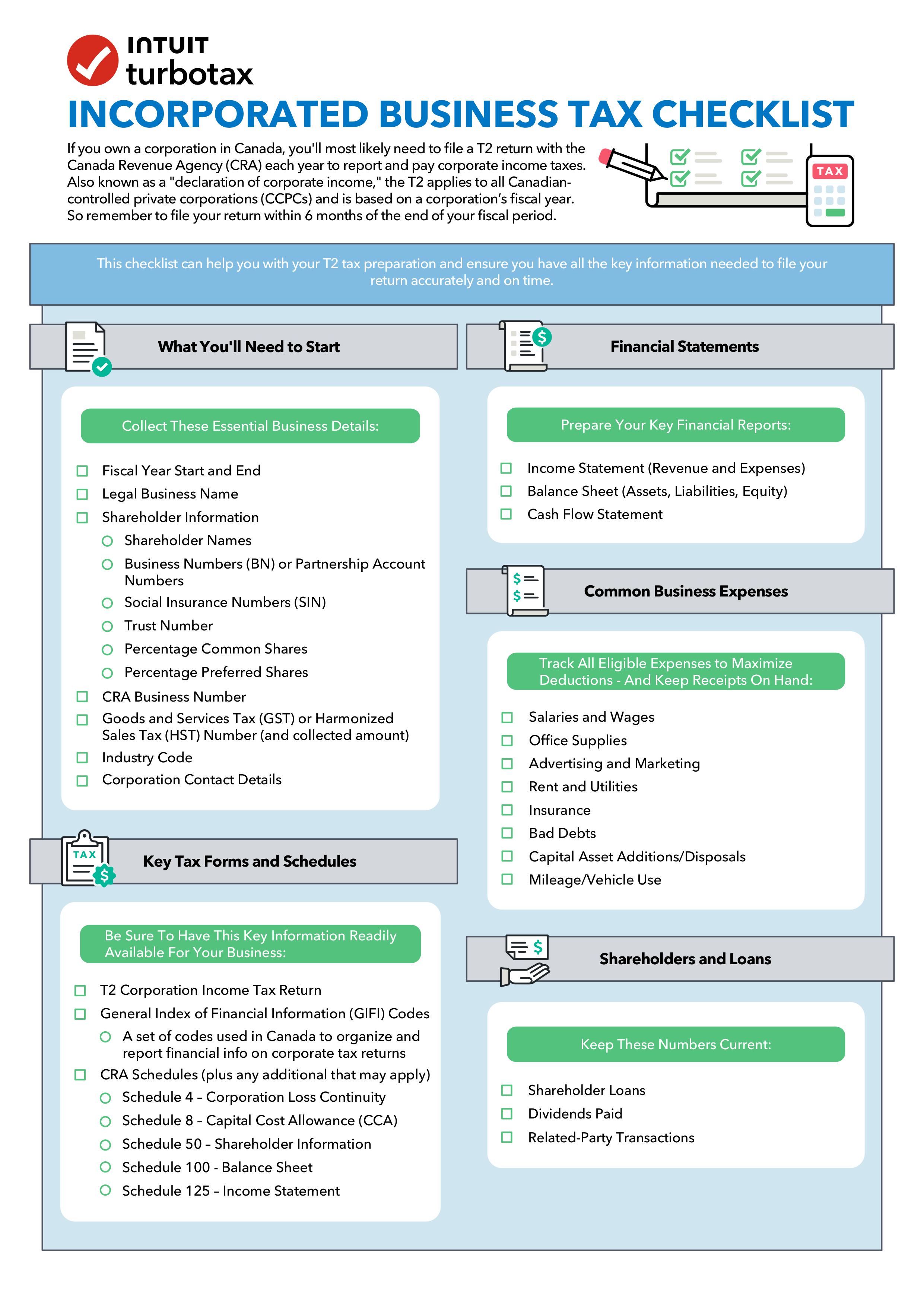

The ultimate checklist to file your corporate taxes

Get organized to confidently tackle your taxes. This tax checklist tells you everything you need to file your corporate return on time and accurately.

Download Checklist

© 1997-2024 Intuit, Inc. All rights reserved. Intuit, QuickBooks, QB, TurboTax, Profile, and Mint are registered trademarks of Intuit Inc. Terms and conditions, features, support, pricing, and service options subject to change without notice.

Copyright © Intuit Canada ULC, 2024. All rights reserved.

The views expressed on this site are intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.